Is "Homo politicus Americanus" good Greek / Latin. Is it the right form for a subspecies name? Should "Americanus" be capitalized or not?

My published articles are archived at iSteve.com -- Steve Sailer

Is "Homo politicus Americanus" good Greek / Latin. Is it the right form for a subspecies name? Should "Americanus" be capitalized or not?

My published articles are archived at iSteve.com -- Steve Sailer

From "McCain Plans Fiercer Strategy Against Obama" in the Washington Post:

Two other top Republicans said the new ads are likely to hammer the senator from Illinois on his connections to convicted Chicago developer Antoin "Tony" Rezko and former radical William Ayres, whom the McCain campaign regularly calls a domestic terrorist because of his acts of violence against the U.S. government in the 1960s.

But not all that fierce:

The Rev. Jeremiah A. Wright Jr. appears to be off limits after McCain condemned the North Carolina Republican Party in April for an ad that linked Obama to his former pastor, saying, "Unfortunately, all I can do is, in as visible a way as possible, disassociate myself from that kind of campaigning."

My published articles are archived at iSteve.com -- Steve Sailer

As I may have mentioned once or twice, many people assume that because Barack Obama is of mixed ancestry, he naturally identifies with all his ancestral races, as does, say, Tiger Woods or Ward Connerly. In reality, Obama has instead felt the constant need to prove he is black enough.

I'm looking for more examples of this phenomenon of feeling the need, due to your unusual background, to prove you are X enough. Perhaps actress Halle Berry? Maybe Zach de la Roccha of Rage Against the Machine is an example. (Daniel Day-Lewis is an amusing example of something slightly different: a complete insider -- his father was Poet Laureate of England and his maternal grandfather ran England's top movie studio -- who has used all his Method acting skills to convince himself that he is a much-discriminated against Irishman). Or Eamon de Valera of Ireland, although I'm not really familiar with his personality. In a different way, Hitler, Napoleon, and Stalin were all from the peripheries of empire.

I think there must be more. Do you know of any?

My published articles are archived at iSteve.com -- Steve Sailer

- Gov. Schwarzenegger is asking the federal government for a $7 billion emergency loan so he can meet payroll.

- Roughly half the dollar value of foreclosed-upon mortgages is in California, which has 12% of the population.

- California Scheming -- the leader of a real estate fraud ring in Beverly Hills is sentenced to 14 years in jail for buying the lousiest homes on Beverly Hills blocks, then having them appraised like their neighbors. Lehmann Bros., who lost $42 million in the scam, hired a private detective to check up on these guys and found they were inflating appraisals and spending the loans on private jets. This kind of thing was imitated all over Southern California on half-million dollar homes in dumpy neighborhoods with nobody being caught because the losses from fraud were too spread out for anybody to bother burning any shoe leather to check them out. (It makes you wonder how much money would have been saved if Wall Street firms had employed a few hundred Philip Marlowes to gumshoe around California's subdivisions checking up on mortgage applicants?)

As a native Californian, something that I've noticed is an increasing intellectual disconnection between the power centers of the East and the reality on the ground in California. At bottom, this financial crisis is California's fault. But Wall Street and Washington seemed to have no clue what California was like in this decade. Observe, for instance, all the incredulity when I've pointed out the role of Latinos in the housing fiasco.

In the 1960s, it was a cliche that California was where America's future was being test-driven. That has certainly panned out, and yet New York and Washington D.C. strike me as having lost interest in California, and thus have become increasingly oblivious to the future of the country.

A generation ago, New York and DC interest in California was motivated by envy, along with fear that California would someday displace them at the top of the totem pole. That fear has faded as California's future has faded.

Yet, California's fraction of the nation's population has grown since the 1960s, making the state even more important than when it was closely observed.

My published articles are archived at iSteve.com -- Steve Sailer

In recent decades, the U.S. has been globalizing its economy, by cutting tariffs and shipping manufacturing jobs to China, and has been globalizing its population by importing tens of millions of poorly-educated Hispanics with IQs around the global average of 90.

Notice the problem?

People with an average IQ of 90 and a decent work ethic make okay assembly line workers. They don't do well, however, in a knowledge-based post-industrial economy.

If we had wanted to have tens of millions more Hispanics, with their blue-collar capabilities, then we should have kept up the tariffs so there would be decent-paying factory jobs for them.

Or

If we had wanted to have a post-industrial "symbolic manipulation" economy, then we should have kept out the flood of people whose children grow up to have low NAEP scores. (A recent study by sociologists with the UCLA Chicano Studies Center found that only 6% of fourth-generation Mexican-Americans -- i.e., people whose grandparents were born in America -- had college degrees.)

You can successfully globalize your economy or your population, but not both.

My published articles are archived at iSteve.com -- Steve Sailer

From This American Life (thanks to Jerry Pournelle), comes a tale of a society with a distinct aversion to reality checks.

Alex Blumberg: For example, a guy I met named Clarence Nathan. He worked 3 part time, not very steady jobs, and made a total of roughly 45 thousand dollars a year roughly. He got himself into trouble and needed money, so he took out a loan against his house. A big one.

Clarence Nathan: Call it 540 for round figures

Alex Blumberg: And you basically borrowed that from the bank and they didn’t check your income?

Clarence Nathan: Right. It’s a no-income verification loan. They don't do that. It's almost like you pass a guy in the street and say: lend me 540,000 dollars? He says, what do you do? Hey, I got a job. OK. It seems that casual even though there are a lot of papers that get filled out and stuff flies all over with the faxed and emails. Essentially, that's ... that the process.

Alex Blumberg: Would you have loaned you the money?

Clarence Nathan: I wouldn't have loaned me the money. And nobody that I know would have loaned me the money. I know guys who are criminals who wouldn't loan me that and they break your knee-caps. I don’t know why the bank did it. I’m serious ... 540 thousand dollars to a person w/bad credit. ...

Alex Blumberg: This is Glen Pizzolorusso, who was an area sales manager at an outfit called WMC mortgage in upstate New York [that makes loans and then bundles the mortgages and sells them to investment banks to peddle as Mortgage-Backed Securities]. Just to repeat, he was making 75 to a 100 grand a month. That's over a million dollars a year. Glen was just out of college. ...

Glen Pizzolorusso: We lived mortgage. That’s all we did. This deal, that deal. How we gonna get it funded? What’s the problem with this one? That's all everyone's talking about.

Alex Blumberg: And when Glen wasn't working, he was doing his next favorite thing, spending ... preferably in the company of, and this is his term, b-list celebrities:

Glen Pizzolorusso: We rolled up to Marquee at midnight with a line, 500 people deep out front. Walk right up to the door: Give me my table. Sitting next to Tara Reid and a couple of her friends. Christina Aguilera was doing some, I’m-Christina-Aguilera-and-I’m-gonna-get-up-and-sing kind of thing. Who else was there? Cuba Gooding and that kid from Filthy Rich: Cattle Drive. What was that kids name? Fabian Barabia? ...

Alex Blumberg: Glen had five cars, a 1.5 million dollar vacation house in Connecticut, and penthouse that he rented in Manhattan. And he made all this money making very large loans to very poor people with bad credit.

Glen Pizzolorusso: We looked at loans. These people didn't have a pot to piss in. They can barely make a car payment and we're giving them a 300, 400 thousand dollar house.

Alex Blumberg: But Glen didn't worry about whether the loans were good. That's someone else's problem. And this way of thinking thrived at every step of this mortgage security chain. A guy like Mike Francis, from Morgan Stanley, he told me he bought loans, lots of loans, from Glen's company, and he knew in his gut they were bad loans. Like these NINA loans.

Mike Francis: No Income No Asset loans. that's a liar's loan. We are telling you to lie to us. We're hoping you don't lie. Tell us what you make, tell us what you have in the bank, but we won't verify? We’re setting you up to lie. Something about that feels very wrong. It felt wrong way back when and I wish we had never done it. Unfortunately, what happened ... we did it because everyone else was doing it.

Alex Blumberg: It's easy to ignore your gut fear when you are making a fortune in commissions. But Mike had other help in rationalizing what he was doing. Technological help. Mike sat at a desk with six computer screens, connected to millions of dollars worth of fancy analytic software designed by brilliant Ivy league math geniuses hired by his firm, which analyzed all the loans in all the pools that he bought and then sold. And the software, the data ... didn’t seem worried at all:

Mike Francis: All the data that we had to review, to look at, on loans in production that were years old, was positive. They performed very well. All those factors, when you look at the pieces and parts. A 90% NINA loan from 3 years ago is performing amazingly well. Has a little bit of risk. Instead of defaulting 1.5% of the time it defaults at 3.5% of the time. That’s not so bad. If I’m an investor buying that, if I get a little bit of return, I’m fine.

Adam Davidson: Wait Alex. I want to step in for a moment because this is a very important piece of tape. A big part of this story, of this whole crisis, is that a lot of really smart people, people who knew better, fooled themselves with this data. It was the triumph of data over common sense. Can you play that tape again?

Mike Francis: All the data that we had to review to look at, on loans in production, that were years old, was positive.

Adam Davidson: As we now know, they were using the wrong data. They looked at the recent history of mortgages and saw that foreclosure rate is generally below 2 percent. So they figured, absolute worst-case scenario, the foreclosure rate may go to 8 or 10 or 12 percent. But the problem with is there were all these new kinds of mortgages, given out to people who never would have gotten them before. So the historical data was irrelevant. Some mortgage pools, today, are expected to go beyond 50 percent foreclosure rates.

In retrospect, the basic political-economic idea of the decade was that the financial elites would wind up with all the financial assets while the masses would be kept pacified with lots of nice consumer gadgets and big houses paid for by borrowing from the financial elites. A foolproof plan!

The key issue is that there was nothing going on in America in this decade that would suggest that below, say, the 75% percentile that human capital -- and thus the ability to earn income and to repay debt -- was increasing. Or was ever likely to increase.

In fact, the signs pointed toward a declining per capita ability to pay as the U.S. became increasingly Hispanic. But, no, you couldn't talk about that in polite society. Instead, we had an increasingly diverse, vibrant society so we must have an increasingly diverse, vibrant economy.

Ideas have consequences.

As various commenters have been suggesting, now that the government is going to, more or less, buy up the unaffordable mortgages on all those Real Homes of Genius in California, Arizona, Nevada, and Florida, you will soon be hearing from the Establishment that ram-rodded the bailout through, and its loyal media, that the only real solution is to let in a lot more immigrants to buy up all those homes. (Of course, as soon as they step off the plane, they'll immediately qualify for all sorts of affirmative action benefits.)

Let me just point out that 50% of the foreclosures and, probably, 75% of the dollar value of foreclosures, have happened in those four high immigration states. That's not a coincidence.

My published articles are archived at iSteve.com -- Steve Sailer

With the passage by the House and the signing by President Bush of the $810 billion bailout bill, you are now (or soon will be) the proud owner of ... well, nobody seems to know what exactly. All you can be sure of is that it will be a bunch of stuff that nobody would buy with their own money.

My published articles are archived at iSteve.com -- Steve Sailer

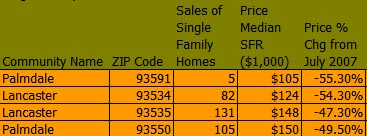

The Dr. Housing Bubble blog has been making this point for a long time about California real estate. For example:

Lowest priced homes in Los Angeles County in July 2008:

Palmdale and Lancaster are in the high desert about 60-75 miles north of downtown LA. Home prices were cut in half there from 2007 to 2008.

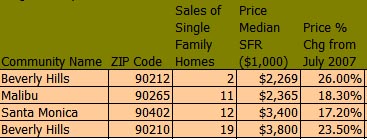

Let us now take a look at these top 4 zip codes in median home price in LA County, where prices were still rising as of July 2008:

ANNOUNCER: Bud Light presents real men of genius. Real men of genius. Today, we salute you, Mr. Giant Taco Salad Inventor.

UNIDENTIFIED MALE: Mr. Giant Taco Salad Inventor.

ANNOUNCER: Ground beef, refried beans, guacamole, cheese, sour cream, and if there's any room left, a few shreds of lettuce. A culinary creation that baffles the human mind. A 12,000-calorie salad. Ay carramba. Some may ask, is your taco salad healthy? Of course it is, it's a salad, isn't it? [If you're still hungry] you can eat that deep fried crunchy bowl.

There are 88 different cities in LA County, which is home to over 3% of the country's residents, and nobody can be expected to know, say, Bellflower from Bell Gardens. So, I'll stick to Real Homes of Genius from one low-end municipality that you might have heard of, Compton, home of the Crips gang. This is where the original West Coast gangsta rappers, NWA, were straight outta. Although world-famous as a black ghetto, already by the time of the 2000 Census, it was 56% Hispanic and no doubt was increasingly Latino all through the Housing Bubble.

(When you're looking at these prices below, add a one or two or three hundred thousand to get prices for comparable homes in cruddy nearby neighborhoods that didn't have a nationally notorious brand name.)

Here, for example, is an 828 square foot manse on a 5,000 square foot Compton lot, with one bathroom, built in 1954.

With the inherent value of this kind of asset, is it any surprise that this 828 square foot Compton home's selling price went up, up, up:

On 11/05/2003, it sold for $110,000.

On 9/30/2004, it sold for $235,000.

On 12/22/2005, it sold for $310,000.

- one bath Compton house built in 1939.

- one bath Compton house built in 1939. square foot Compton home. Dr. Housing Bubble explains:

square foot Compton home. Dr. Housing Bubble explains:This 1,089 square foot home includes four bedrooms and two “full” baths. Nestled in the majestic resort town of Compton, you will entertain your friends and family behind U.S. Steel reinforced gates, such as those guarding the Rockefeller Estate. This home uses transcendent features of the 1950s including a patented aqua green color to ward off nuclear attacks from Soviet warships. This moderately priced dream crib is all yours for the rock bottom price of $375,999. This is actually less than the sale price of 2006:What happened to all the money that people in Compton made selling these Real Homes of Genius to each other? A few wise oldtimers presumably bailed out and retired to the South with the profits from selling their Compton homes to Hispanic newcomers. A few clever youngsters probably sold out at the peak and rented homes for $900 per month. A lot of the money, of course, went into buying new Real Homes of Genius. But, I suspect the worst problem is that a lot of people wound up spending the money on consumer goods. In fact, plenty of people probably spent money they assumed they'd make eventually off selling their homes to support a lifestyle that can't be supported. And that's going to require a nasty contraction of the real economy to work out.

Sale History

06/23/2006: $412,000

10/01/1981: $58,500

My published articles are archived at iSteve.com -- Steve Sailer

In the LA Times today, Warren Buffett endorsed the bailout plan as "a rescue plan for America." He went on to say:

"If we could do the deal that is available to the United States government and have its staying power, and its borrowing costs, we would make significant money. I would love to have, if they buy the assets at market price, I would love to have 1% of the profit or loss that results from buying these assets from troubled financial institutions."

Okay, well, that suggests a second deal:

I hereby offer to sell, straight up, my family's share of the bailout, both payouts and subsequent profits, to Mr. Warren Buffett. If he'll write me a check for what it will cost me in taxes, I'll sign over to him my share of the profits, if any.

Seriously, if Buffett really "would love to have 1% of the profit or loss that results from buying these assets from troubled financial institutions," then I am all in favor of him ponying up $7 billion for 1% of the action.

Indeed, I would be feeling a lot better about this deal if Buffett, his buddy Bill Gates, and the rest of the Forbes 400 put together a syndicate to, say, buy 2/7th of the bailout for $200 billion dollars. I'd love for them to have a say in how it's spent as long as they had substantial skin in the game. Buffett has been investing billions in Goldman Sachs and GE in return for 10% interest and warrants to buy stock at certain prices. I'd trust Buffett to come up with a better bailout plan than Paulson or Congress ... but only if Buffett had billions riding on it himself.

By the way, Buffett offers a caveat on his prediction:

"If they buy them at market, they will realize a significant profit over time . . . but the key is buying at market prices."

Indeed. But if they buy them at market prices, how do insolvent banks get bailed out?

I'm guessing about $2 to $2.5 trillion in paper wealth has evaporated in California houses alone, with similarly scaled losses in the other 49 states' houses.

On top of that, there's a possibility that those losses in wealth would be much bigger if the entire financial system comes tottering down because of the mortgage meltdown and we go back to an economy based on trading salt for rifle cartridges.

But, preventing that general collapse isn't going to make those 4 to 5 trillion in paper losses go away. That wealth isn't coming back in the real world because that wealth never really existed.

Now, the big question that I haven't seen answered is: How much of the 4 to 5 trillion was wasted on consumer crap during the bubble as if it were real? I don't know. Personally, I didn't spend more during the Bubble because I never believed in the Bubble price for my home. But, I'm driving a 1998 Accord with 105,000 miles on it, while a lot of other people on the freeway are driving 2008 Lexuses with $4,000 rims, so it seems as if other people took the market price of their homes more on faith.

So, I'm left wondering whether $700 billion (or, I guess, $810 billion in the Senate's version) is going to be enough to prevent a collapse of the financial system?

UPDATE: So, how do you price financial assets if the market has locked up? I have no idea what to do with all the derivatives and other financial black magic, but the underlying mortgages aren't that complicated. The good news is that rents weren't much affected by the bubble. Rents tend to trend upward at a fairly stable rate over the years. In California, house purchase prices got wildly out of wack with house rents. We also have readily available on the Internet a vast amount of information on rental properties comparable to each mortgaged house -- Dr. Housing Bubble typically looks at a half dozen comparable rental units for each of his Real Homes of Genius awards.

So, it wouldn't be that hard to come up with a relatively simple spreadsheet to value homes based on rents in that area. From that, the government could value mortgages. One big technical problem might be reassembling sliced and diced mortgages. But the biggest problem is that 4 or 5 trillion in wealth just vanished and some unknown fraction of that has already been spent.

My published articles are archived at iSteve.com -- Steve Sailer

Steven Erlanger writes in the NYT:

They value sophistication above almost anything, and so they regard their own hyperactive president, Nicolas Sarkozy, with his messy romantic life and model-singer wife, as “Sarko the American.”

But this year has been difficult for the French. Mr. Sarkozy has generally supported American foreign policy and has praised the United States’ openness and entrepreneurial verve. And the sudden emergence of Senator Barack Obama — black, and seen as elegant and engaged with the larger world — has sent many French into a swoon.

But the combination of two recent surprises — Gov. Sarah Palin and America’s terrifying financial meltdown — has brought older, nearly instinctual anti-American responses back to the surface.

These two surprises, one after the other, have refreshed clichés retailed under President Bush, confirming the deeply held belief of the French that the United States remains the frontier, led by impenetrably smug and incurious upstarts who have little history, experience or wisdom.

Even worse, from the French perspective, Americans are reckless optimists, incurably blind to the tragedy of life, to the weary convolutions of history and thus to the need for lengthy August vacations and financial regulations.

While the French see themselves as the heirs of urban revolutionaries, with a strong distaste for politicized religion, the American revolutionary spirit seems to them these days to come like a hurricane from the uncosmopolitan right — from the dry, dull flatlands of Texas ranch country or the emptiness of Vice President Dick Cheney’s Wyoming, and now from the odd sunset communities of Arizona and the bizarre bars, churches and hockey rinks of Alaska.

The financial meltdown also seems inevitably American, a product of the reckless audacity that the French pretend to abhor, but often secretly admire. But however careful France’s own banks may have been, the United States is so large and so dominant that the French are afraid of being hit with what one economist, Daniel Cohen, called the “toxic waste” of the scandal.

This year, mocking the candidates has become an industry, with the satirical puppet show “Les Guignols de l’Info” recently adding a squeaky-voiced Senator John McCain puppet to the jug-eared Obama model. In general, though, Americans are portrayed as Sylvester Stallone, lunky and thick-headed. Ms. Palin has been a kind of godsend.

The French know exactly what to make of her, said Frédéric Rouvillois, and that is the problem. Ms. Palin may be an American dream but she is a French nightmare, said Mr. Rouvillois, a lawyer and social historian who has just written a book titled “The History of Snobbery.”

“She’s a caricature of a certain America that hasn’t parted with its boorish ‘Wild West’ side,” said the impish Mr. Rouvillois, who has also written a history of good manners. “For the French snob, the only admissible American is from the East Coast, knows Henry James, is comfortable in French, a sort of European on the other side of the Atlantic.”

A little, yes, like Senator John Kerry. ...

France, like most of Europe, is quite taken with the Democratic candidate, whom the French regard as a “métis,” politely translated as someone of mixed race, usually used for those of African colonial ancestry. Mr. Obama is seen uniquely as an American métis with global experience and antecedents in Africa, through his Kenyan father, not in slavery.

Bernard-Henri Lévy wrote in the magazine Le Point of Mr. Obama as a new type of American black politician.

“Obama is, certainly, black,” Mr. Lévy wrote. “But not black like Jesse Jackson; not black like Al Sharpton; not black like the blacks born in Alabama or in Tennessee and who, when they appear, bring out in Americans the memories of slavery, lynchings and the Ku Klux Klan — no; a black from Africa; a black descending not from a slave but from a Kenyan; a black who, consequently, has the incomparable merit of not reminding middle America of the shameful pages of its history.”

He goes on for a while, but you get the idea.

My published articles are archived at iSteve.com -- Steve Sailer

The bald and square-jawed Ed Harris has played American heroes and psycho killers since first drawing notice as astronaut John Glenn in 1983's "The Right Stuff." He's now written and directed "Appaloosa," an amiable Western about masculine camaraderie and honor adapted from the book by Robert B. Parker, the genre novelist who created Spenser, the Boston private eye. "Appaloosa" furnishes Harris and Viggo Mortensen (the King in "The Return of the King") with plenty of wry lines for their portrayals of itinerant lawmen in the New Mexico of the 1880s.

Fish do not feel wet, we are told (although on what authority, I cannot say), and cowboys and Indians movies once felt no more awkward than cops and robbers films do today. Westerns were then less a genre than a natural, default mode.

In the early 1970s, however, urban crime dramas, such as "The French Connection" and "The Godfather" replaced Westerns as the norm. The Western has since become a highly self-conscious genre, one almost immobilized by the weight of its pre-1970 cinema history.

As an actor, however, Harris appears unburdened by all the film school baggage the Western has accumulated. The straightforward "Appaloosa" provides two outstanding roles and sundry old-fashioned pleasures.

My published articles are archived at iSteve.com -- Steve Sailer

A couple of weeks back, I suggested that Obama mention that he plays poker while McCain likes to roll the dice, poker being a game of skill while craps is, well, a crapshoot. Earlier this week,

I read the other day that Senator McCain likes to gamble. He likes to roll those dice. And that's okay. I enjoy a little friendly game of poker myself every now and then.

But one thing I know is this -- we can't afford to gamble on four more years of the same disastrous economic policies we've had for the last eight.

I know that when Senator McCain says he wants to bring the same kind of deregulation to our health care system that he helped bring to our banking system -- his words -- well, that's a bet we can't afford. We can't afford to roll the dice by privatizing Social Security, and wagering the nest egg of millions of Americans on Wall Street. We can't afford to gamble on more of the same trickle down philosophy that showers tax breaks on big corporations and the wealthiest few. We've tried that. It doesn't work.

My published articles are archived at iSteve.com -- Steve Sailer

One of the problems we've all had in discussing the racial angle of the mortgage meltdown is the lack of good data.

Since writing that fairly comprehensive article on Saturday, I've also found some seemingly trustworthy statistics on recent subprime loans by ethnicity. (Unfortunately, nobody seems to have calculated defaults by ethnicity. Perhaps nobody wants to know?)

We do know that defaults are closely tied to subprime loans. The most toxic of all, adjustable rate mortgage (ARM) subprime loans, accounted in early 2008 for only six percent of all loans outstanding but 39 percent of foreclosures started. Fixed and adjustable subprimes account for only 12 percent of loans outstanding, but half of current foreclosures. The subprime share of new lending roughly doubled from 2003 to 2004 and increased again in 2005. So far, that's where most of the "unexpected" defaults have come from, although the default contagion will likely spread to lower interest rate adjustable rate mortgages in the near future.

Compliance Tech, a firm that helps lenders "Manage Diverse Lending Markets," estimates that in 2004-2006, minorities accounted for 44 percent of all subprime loans, with Hispanics slightly outnumbering blacks.

The numbers we really want, though, are defaults, dollar value of defaults, and incremental dollar values of defaults over expected levels.

Minorities with subprime loans probably have higher default rates than whites with subprime loans. For example, default rates on college loans are about five times higher for blacks, and more than two times higher for Hispanics, than they are for whites. (Asians are best of all at paying back college loans.) Normally, college loans are handed out more willy-nilly than mortgages, so the ethnic default rate gaps likely aren't as big in mortgages, but willy-nilly pretty much describes 2004-2006 mortgage lending in some markets.

My published articles are archived at iSteve.com -- Steve Sailer

I want to expand on something I mentioned briefly in my last VDARE.com article on Karl Rove and the mortgage disaster. Sorry if some of it already appeared in VDARE, but the full thing will help the residents of the two polar states understand each other's situation better.

In defense of Bush and Rove, it was natural for them to misunderestimate the financial scale of what they were propagating because they are from Texas, where land prices have been saner than in California ever since the bursting of the first oil bubble a quarter of a century ago. At present, Texas ranks only 15th out of 50 states in per capita foreclosure rate, far below most other highly Latino states. That's because land costs in Texas are dramatically lower than in most other states with heavy Hispanic concentrations, keeping recent homebuyers from getting in over their heads so badly. I visited San Antonio in April 2007, at the height of the housing bubble, and saw billboards advertising new 3000 square foot, five bedroom homes for $162,000.

In the flat, well-watered eastern half of Texas, there's an enormous supply of buildable land. Moreover, there aren't many environmental or other restrictions on home development. In contrast, California has a thin strip of exquisite coastal land, mostly locked down tight by strict environmental controls, backed by uninhabitable mountains. The level inland areas become increasingly miserable for year-round habitation the farther east you go (for example, the aptly named Death Valley). Likewise, Nevada and Arizona have significant water limitations, restricting growth to certain areas.

Texas Republicans are prone to blame the limited supply of housing in California on leftwing Not In My Back Yard politics used by greedy homeowners to raise their home values and keep out undesirables. Some of that is true, but there are topographical reasons for limiting development in mountainous California, such as smog and traffic, that aren't easily understood on the Texas prairie.

For instance, the northern exurbs of Los Angeles County, the Santa Clarita Valley, are connected to Los Angeles almost solely by Interstate 5 through the rugged Newhall Pass. The only proposed alternative to this chokepoint would require colossally expensive tunneling through 15 miles of the earthquake-prone San Gabriel Mountains. So, the current residents of the Santa Clarita Valley, who tend to be more Republican than Los Angelenos, raise a stink about exacerbating commute times to their jobs in LA whenever anybody asks for approval of a new development. Thus, the posh Valencia TPC golf and housing development was proposed in 1985 but construction didn't begin until 2000. Other planned developments have been vetoed after long years of hearings.

Therefore, in California, unlike in Texas, it takes many years for increases in housing supply to catch up to increases in demand. That's why the loose credit policies of the Bush years turned into higher home prices in California than in Texas. To be precise, a Los Angeles home averaged 2.6 times the price of a Dallas home in 2001 and 4.7 times in 2005. Even in 2005, the median Dallas home only cost a sane 2.8 times the local annual income, while the median Los Angeles home cost a ridiculous 12.7 times what the median Angeleno was making.

From Bush & Rove's Texas-centric point of view, if some guy named Juan with no assets besides a 1979 Datsun pickup truck gets a liar loan for a house in Texas, his mortgage is, what, $100,000? He might be able to scratch together enough money to meet his payments. If he can't, well, Juan is gone, but that's just $100,000 down the drain. No biggie, Bush and Rove would assume.

What they apparently didn't realize in 2001 was that when his cousin Jose, who is equally broke, gets a mortgage in California, that was, say, $200,000. And by Bush's second term, the Administration's easy money-easy credit "affordable housing" policies meant Jose had to worm his way into a $400,000 mortgage to get a crummy house in California. No way, Jose is going to be able make the monthly payment after his two-year teaser rate runs out. And when he defaults, that's $400,000 down the rathole.

My published articles are archived at iSteve.com -- Steve Sailer

My published articles are archived at iSteve.com -- Steve Sailer

Let me suggest a conceptual distinction to make things clearer.

Economically, we face two related but distinguishable problems.

First, due to post-modern financial engineering, Wall Street has created vast upside down pyramids of leverage that are so intricate that nobody is sure what financial instruments are worth anymore, with frightening implications for the whole system, which could cause a lock-up of all lending.

Second, we have a fundamental problem, which is that a lot of those highly leveraged complex instruments really aren't worth much because the basic assets they balance on top of have declined sharply in value. Essentially, in this decade home prices (primarily in a small number of states, most notably California, Nevada, Arizona, and Florida) inflated to absurd levels, generating trillions in new wealth on paper. Those gains are now gone and won't come back for decades because they were always stupid: there was never enough human capital in California to earn enough money to pay for those houses.

My published articles are archived at iSteve.com -- Steve Sailer

Invited members of the Great and the Good had spent a few days in a conference room, where they decided to give the Treasury Secretary power to give away $700 billion dollars.

But then, this quaint body called the House of Representatives (which I believe is mentioned somewhere in the Constitution) had the gall to vote against it, 228-205. Don't these mere elected representatives understand how many gallons of diet soft drinks the self-appointed authors of the bailout had consumed over the last two weeks?

My published articles are archived at iSteve.com -- Steve Sailer

With the financial crisis, we might start seeing a few more defaults in Greenwich, CT (we can all hope, can't we?), but so far, the defaults have tended to hit marginal areas hardest. Here in California, people in Santa Monica aren't defaulting, it's the poor bastards out in the high desert or even down in Bakersfield in the hot, smoggy Central Valley.

In these godforsaken places, all sorts of mini-McMansions have gone up on the theory, apparently, that, hey, they're in California! Every peon in Guatelombia has seen Baywatch and wants to move to California (even though Lancaster, CA looks more like Death Valley Days). So prices can only go up, up, up!

Imagine you're a homeowner in Santa Clarita in 2005, now a nice established exurb 35 miles north of LA. You bought your house in 1995 at the bottom of the market for $175,000 and a decade later it's worth three or four times that much. You can take cash out with home equity loans, so why not find an investment property?

Of course, you'll have to look farther out, deeper into the dusty high desert, like in Lancaster, 70 miles from downtown LA. They're building many new 3,000 s.f. homes on culdesacs with all the amenities. You should buy one up now and resell it when new refugees from the LA Unified School District arrive.

The family you sell it to will, no doubt, be moving to the exurbs to get their kids away from all the Guatelombians in the LA public schools. It's not like Bush is going to close the borders and stop the flood of Guatelombians. So, there will always be refugees looking for "good schools."

That's one reason, you realize, why these new homes in the exurbs tend to be so big -- they're expensive in the hopes of discouraging low rent people from moving in next door. Sure, they cost a fortune to air condition during Lancaster's summer (March-October), but it's all in a good cause.

You start shopping around outside Lancaster. The Cypress Creek Estate sales agents talk about the new high school that's going to be built to serve these new neighborhoods. It will be diverse, but not too diverse, if you know what I mean. Two-thirds white, one fifth Hispanic, enough Asians to show your neighborhood's a good investment, enough blacks so that the football and basketball teams will be competitive. Sounds good!

You get the feeling that there aren't any cypress trees within 100 miles or creeks within 20 miles, but that's not the point. The point is that with low down payment mortgages available, you have all sorts of speculative options available. For example, with a 3% down payment, you could buy a new $400,000 house in a development of 3000+ square foot homes for only $12,000 in cash (not counting the usual points and fees). So, why not buy two? Only $24,000!

If each house goes up 10% in value the first year you own them, you've made $56,000 on your $24,000 investment. Try getting that rate of interest on a CD. Leveraging 33 and 1/3 to one does wonders for your ROI.

Granted, that's exaggerated because you have to pay the monthly mortgage, but you can get a two year teaser interest rate that makes things easier. You're going to be cashing in before two years are up!

Of course, that assumes you can flip them, which often turns out to be more difficult than you initially anticipated. After all, when such easy profits can be made, builders build. Sure, the ecology rules slow them down for years, but in Lancaster there really isn't a whole lot of ecology other than scorpions stinging each other, so eventually a flood of new housing comes online.

Then, there's the problem that not too many people actually deeply, truly want to live in Lancaster, unless they have a job there. Back in the Cold War, there were good jobs at Edwards Air Force base and in aerospace plants. There still are, but nobody's too sure why, or exactly how long the federal government will go on funding new fighter planes to fight ... well, nobody's too sure who.

So, most of the new jobs there are building more houses for Even Greater Fools. Or, you could get work standing by the side of the road as a Human Sign, twirling a big arrow to attract attention to the new housing developments. (Here's my 2005 VDARE article on Human Signs as the personification of the Expensive Land / Cheap Labor economy.)

So, the flipping goes a little slower than you expected. And even at the teaser rate, the monthly on those two empty houses is starting to gnaw away at your net worth. What do you do? What do you do?

Well, you could always rent it out until the market takes off again like you know it will.

But that raises the question of who exactly would want to rent in Lancaster, when you can buy a home in Lancaster for $12,000 down, or you can rent for a reasonable rate in the San Fernando Valley, 40 miles closer to work and 15 degrees cooler, with no dust storms.

Q. So, who wants to live for awhile in Lancaster?

A. The Guatelombian construction workers who are building all the new McMansions down the road.

So, you get some bunk beds and rent out your five bedroom house to 12 Guatelombians. They work hard all day and pay on time. Sure, the neighbors are complaining because your tenants are drunkenly singing along to mariachi music in the backyard all weekend and one fellow got a little too celebratory and started shooting his gun in the air. But, you don't live next door to them, so what do you care?

And then you rent your other house to a couple of families of Guatelombian construction workers. The parents are fine, but you start to notice grafitti around the neighborhood. There are rumors of a gang shooting at the strip mall.

But the money is good in the meantime while you're getting closer to your big payday.

But then you notice that the nice quiet street isn't so quiet anymore. The other speculative owners are doing the same thing you did: renting to construction workers. Soon, there are cars up on jacks on front lawns and Cypress Creek Estates is a big Guatelombian slum. If only you had done it, it would have been okay. But once all those other jerks followed your example, you were hosed. Now, nobody wants to buy into Cypress Creek Estates.

After awhile, they stop constructing new homes in Lancaster, so some of your tenants go home to Guatelombia, while the others hang around Home Depot looking for day labor. It gets harder to collect your rent. So you toss out the construction workers and bring in a Section 8 family. The great thing about Section 8 is that you get your rent checks straight from the federal government, so you don't have to go knock on the door, because, well, to be honest, your new tenants haven't (a single grandmother of 38, her three daughters and their three children, plus a fluctuating cast of boyfriends) don't seem as polite as the Guatelombians.

My published articles are archived at iSteve.com -- Steve Sailer

Penn Bullock has the first press interview with an executive officer of AEY, Inc., the Miami Beach weapons dealership charged with defrauding the Pentagon and the Afghan Army in a $200 contract using old made-in-China ammunition from Albania, etc etc (you know the story).

When MicroCOSM is released in a few weeks, [David] Packouz will almost certainly be the world's first and only rocker-cum-masseur-cum-arms-dealer.

My published articles are archived at iSteve.com -- Steve Sailer

Rather than mention all the great performances Paul Newman gave, I'd like to recall a role he chose to give up.

One of my favorite movies is John Huston's version of Kipling's short story "The Man Who Would Be King." It was in Development Hell for 20 years, going through multiple screenplays. Originally, Huston was going to direct Clark Gable as the majestic Daniel Dravot and Humphrey Bogart as the sly Peachy Carnehan. I'm not sure if the stars were going to attempt English accents, or if they were going to be turned into Canadians in the Indian Army, or what.

Then Bogie died. After his comeback in the "Misfits," Gable wanted to revive the project, so Huston was looking for a new co-star, when Gable had a heart attack and died. In the 1970s, the project got relaunched, with Paul Newman and Robert Redford attached. (I'm guessing with Redford as Danny and Newman as Peachy, but Newman being older and almost as handsome as Redford would have made casting more flexible and/or confusing than with Gable and Bogart, where there was never a doubt who would play which role.) John Huston and his secretary, Gladys Hill, wrote a great fourth script.

From director John Huston's autobiography "An Open Book:"

"I sent the new screenplay to Paul, who called me immediately and said it was one of the best things he'd read, but he'd had second thoughts about the casting of the leads, which at that point were to have been himself and Robert Redford. He said they should be played by two Englishmen. Paul, speaking not as an actor but as someone interested in the improvement of the breed, cast it right there: "For Christ's sake, John, get Connery and Caine!"

Screenwriter William Goldman's book Adventures in the Screen Trade includes a fair amount of malicious gossip about the swelled heads of big stars he'd written for, such as Redford and Dustin Hoffman, but he only had praise for Newman as a human being.

My published articles are archived at iSteve.com -- Steve Sailer

On VDARE.com, I point out the name of a man who has so far escaped any blame for the mortgage meltdown, but who deserves a share. Indeed, you might almost call him "The Architect."

It's a big article, and you'll notice it tends to turn into a sort of Unified Field Theory of iSteve obsessions. I had fun pulling it all together and I hope you have fun reading it.

My published articles are archived at iSteve.com -- Steve Sailer